Advertisements

Advertisements

Question

Answer the following question:

The market for a good is in equilibrium. How would an increase in an input price affect the equilibrium price and equilibrium quantity, keeping other factors constant? Explain using a diagram.

Solution

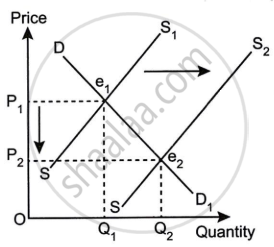

An increase in input price results in decreases in the supply and no change in demand. The given figure shows how would an increase in an input price affect the equilibrium price and equilibrium quantity:

The market supply falls with the rise in the input prices. As a result, the supply curve shifts parallelly leftwards to S2S2 from S1S1. Thus, at the initial price OP1, holding demand unchanged, there exist excess demand equivalent to (Oq1 – Oq1') units of output. This excess demand will lead some of the consumers to pay a higher price in order to obtain the extra units of output. The rise in the market price will continue until it reaches OP2, where the new supply curve S2S2 intersects the initial market demand curve D1D1. The new equilibrium is established at point E2 with the equilibrium price as OP2and equilibrium output as Oq2. At the new equilibrium, the equilibrium price has risen, whereas, the equilibrium quantity has fallen.

To summarise,

Decrease in supply(due to a rise in the input prices) ⇒ Excess demand at the existing price ⇒ Rise in the price level ⇒ New equilibrium ⇒ Rise in price and fall in quantity demanded.

APPEARS IN

RELATED QUESTIONS

Determination of equilibrium price under perfect competition.

Explain the chain effects, if the prevailing market price is below the equilibrium price.

If the prevailing market price is above the equilibrium price, explain its chain of effects.

Explain the chain of effects of excess supply of a good on its equilibrium price

X and Y are complementary goods. The price of Y falls. Explain the chain of effects of this change in the market of X.

Explain the chain of an effect of excess demand of a good on it equilibrium price.

Distinguish between Gross domestic product at a market price and Gross domestic product at factor cost.

Equilibrium price of an essential medicine is too high. Explain what possible steps can be taken to bring down the equilibrium price but only through the market forces. Also explain the series of changes that will occur in the market.

Define or Explain the General equilibrium.

Define or explain the following concepts (Any THREE):

Effective demand

At what level of price do the firms in a perfectly competitive market supply when free entry and exit is allowed in the market? How is the equilibrium quantity determined in such a market?

Define or explain the following concept:

Price discrimination

State whether the following statement is TRUE and FALSE.

Under perfect competition, price is determined by equilibrium of demand and supply.

Fill in the blank with appropriate alternative given below

The price at which demand and supply equate to each other is called _______ price.

Suppose the demand and supply equations of a commodity X in a perfectly competitive market are given by :

Qd = 1700 – 2P

Qs = 1300 + 3P

Calculate the value of equilibrium price and equilibrium quantity of the commodity X.

State whether the following statement is true or false. Give reasons for your answer :

When the equilibrium price is greater than the market price there will be excess supply in the market.

The diagram given below shows the change in price of cotton shirts. Which one of the following causes the equilibrium price to move from P1 to P2?