Advertisements

Advertisements

Question

Explain the conditions of producer's equilibrium under perfect competition.

Solution

Producer’s Equilibrium is defined as a state where a producer is earning maximum possible profit by producing a particular level of output. It is referred to as 'equilibrium' because a producer has no incentive to move away from this point, as such deviation will reduce his/her profit. Under perfect competition, there are two approaches to attain Producer's Equilibrium viz.

1. TR-TC Approach

2. MR-MC Approach

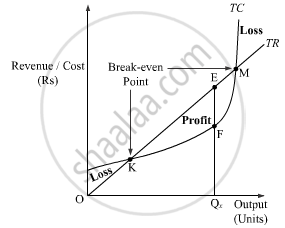

TR-TC Approach

According to this approach, a firm (or a producer) maximises its profit, where the difference between TR and TC is the maximum i.e.

Profit (π) = TR – TC

where, π represents Profit

TR represents Total Revenue

TC represents Total Cost

MR-MC Approach

According to this approach, the firm (or producer) will attains its equilibrium, where the following two necessary and sufficient conditions are fulfilled.

1. Necessary Condition or First Order Condition (FOC)

or,

2. Sufficient Condition or Second Order Condition (SOC)

Slope of MC > 0

APPEARS IN

RELATED QUESTIONS

From the following information about a firm, find the firms equilibrium output in terms of marginal cost and marginal revenue. Give reasons. Also find profit at this output

| Output (units) | Total Revenue (Rs) | Total Cost (Rs) |

| 1 | 7 | 8 |

| 2 | 14 | 15 |

| 3 | 21 | 21 |

| 4 | 28 | 28 |

| 5 | 35 | 36 |

Explain the conditions of producer’s equilibrium with the help of a numerical example.

Explain the conditions of a producer's equilibrium in terms of marginal cost and marginal revenue. Use diagram.

Given below is the cost schedule of a product produced by a firm. The market price per unit of the product at all levels of output is Rs12. Using marginal cost and marginal revenue approach, find out the level of equilibrium output. Give reasons for your answer

| Output (units) | 1 | 2 | 3 | 4 | 5 | 6 |

| Average Cost (Rs.) | 12 | 11 | 10 | 10 | 10.4 | 11 |

Using marginal cost and marginal revenue approach, find out the level of output at which producer will be in equilibrium. Give reasons for your answer

| Output (units) | 1 | 2 | 3 | 4 | 5 | 6 |

| Average Revenue (Rs) | 20 | 20 | 20 | 20 | 20 | 20 |

| Total Cost (Rs) | 22 | 42 | 60 | 76 | 96 | 120 |

Why is the equality between marginal cost and marginal revenue necessary for a firm to be in equilibrium? Is it sufficient to ensure equilibrium? Explain.

Explain why will a producer not be in equilibrium if the conditions of equilibrium are not met.

From the following table, find out the level of output at which the producer will be in equilibrium. Give reasons for your answer.

|

Output (units) |

Marginal Revenue Rs |

Marginal Cost Rs |

|

1 |

8 |

10 |

|

2 |

8 |

8 |

|

3 |

8 |

7 |

|

4 |

8 |

8 |

|

5 |

8 |

9 |

With the help of the given schedule, determine the firm's equilibrium using marginal revenue − marginal cost approach. Give valid reasons in support of your answer.

| Output (in units) |

Total revenue (TR) (in ₹) | Total Cost (TC) ( in ₹) |

| 1 | 20 | 20 |

| 2 | 40 | 30 |

| 3 | 60 | 36 |

| 4 | 80 | 40 |

| 5 | 100 | 60 |

| 6 | 120 | 90 |

Answer the following question.

Explain the conditions of the producer's equilibrium with the help of a numerical example. Use marginal cost and marginal revenue approach.

Fill in the blank.

"For a firm to be in equilibrium, Marginal Revenue (MR) and Marginal Cost (MC) must be __________ and beyond that level of output Marginal Cost must be ____________."

What is meant by accounting cost?