Advertisements

Advertisements

Question

Explain the accounting cycle.

Solution

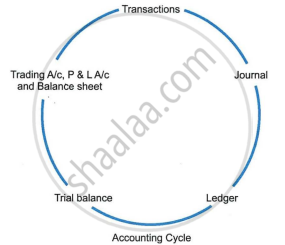

Accounting Cycle

Accounting cycle begins with the recording of financial transactions and ends with the preparation of a balance sheet. It is also called the process of accounting. Accounting cycle consists of the following stages:

- Recording of financial transactions only: In accounting, only those transactions are recorded which can be converted in terms of money. Other transactions, however important they may be, are not recorded, if they cannot be converted in terms of money. A transaction is an external event.

- Recording transactions in journal (journalising): The first book in which the transactions of a business are recorded is called a journal. Here the business transactions are recorded in the order in which they occur. Each record in a journal is called 'entry'. It is also called the book of original entry. A journal is the record which shows the complete story of a transaction in one entry.

- Posting in the ledger: The process of transferring of entries from a journal to the ledger accounts is called posting. A ledger facilitates accumulation at one place of all the information about changes in specific accounts. This results in classification of transactions. All accounts in the ledger are balanced.

- Preparation of a trial balance: Trial balance is a list of balances of all ledger accounts, hence balances from the ledger are transferred to the trial balance. It is an instrument for carrying out the job of checking and testing. The total of credit balances must be equal to the total of debit balances.

- Preparation of income statement: It consists of preparation of trading and of profit and loss account. Trading account is prepared to ascertain the gross profit. A profit and loss a/c tells us about the profit/loss during the period. It is usually prepared at the end of the accounting period.

- Balance sheet: It is a summary of the assets and liabilities existing in a business on a particular date, usually the last day of each accounting year. It is also called position statement. It shows the financial position of a business.

- Opening the new books next year: The balances of assets and liabilities accounts are transferred in the new journal at the beginning of the next financial year. The same process is repeated year to year.

APPEARS IN

RELATED QUESTIONS

Financial position of a business is ascertained on the basis of ___________.

What are the steps involved in the process of accounting?

Ledger is also called the ______.

The accounting cycle consists of ______.

It refers to a complete sequence of accounting activities.

The first step in accounting cycle is ______.

Accounting cycle ends with the ______.

What is accounting cycle?

Every transaction has four effects on accounting records. Give two reasons either for or against.

State four stages of Accounting cycle.