Advertisements

Advertisements

Question

How do the equilibrium price and the quantity of a commodity change when price of input used in its production changes?

Solution

The change in the price of input alters the cost of production of a commodity.

Let us analyze the two different cases.

-

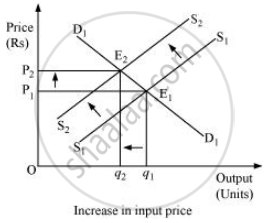

Increase in input price

If the input price of a firm increases, the cost of production will also increase, which will discourage the firm’s incentive to produce and supply the commodity. This will lead to a left upward shift of the marginal cost curve, which further will lead to a leftward parallel shift of an individual firm’s supply curve and finally a leftward shift of the market supply curve. The demand curve remaining the same, the new equilibrium will occur at E2 with higher equilibrium price (P2) and lower quantity of output (q2).

-

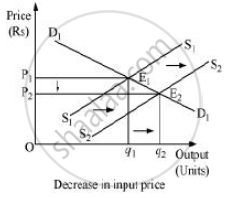

Decrease in input price

If an input price of a firm decreases, then the cost of production will also decrease. This will shift the marginal cost curve rightward, which implies that the firm’s supply curve will also shift rightward. Consequently, the market supply curve will shift rightward parallelly from S1S1 to S2S2. Demand curve remaining the same, the new equilibrium will occur at E2 with lower equilibrium price (P2) and higher quantity level of output (q2).

APPEARS IN

RELATED QUESTIONS

A market for a good is in equilibrium. There is simultaneous "increase" both in demand and supply of the good. Explain its effect on the market price

Market for a good is in equilibrium. There is simultaneous "decrease" both in demand and supply of the good. Explain its effect on market price

A market for a good is in equilibrium. The demand for the good 'increases'. Explain the chain of effects of this change.

What is meant by 'excess supply' of a good in a market?

Explain its chain of effects on the market of that good. Use diagram

Draw average revenue and marginal revenue curves in a single diagram of a firm which can sell more units of a good only by lowering the price of that good. Explain.

Market for a good is in equilibrium. There is an ‘increase’ in demand for this good. Explain the chain of effects of this change. Use diagram.

What will happen if the price prevailing in the market is

(i) above the equilibrium price?

(ii) below the equilibrium price?

How are equilibrium price and quantity affected when income of the consumers increase.

Using supply and demand curves, show how an increase in the price of shoes affects the price of a pair of socks and the number of pairs of socks bought and sold.

How will a change in price of coffee affect the equilibrium price of tea? Explain the effect on equilibrium quantity also through a diagram.

Compare the effect of shift in the demand curve on the equilibrium when the number of firms in the market is fixed with the situation when entry-exit is permitted.

Answer the following question.

Show with the help of diagrams, the effect on equilibrium price and quantity when:

There is a rise in the prices of inputs.

Rate of interest on savings account is more than that on recurring account.